OK I said it. Single tenant triple net lease deals are NOT real estate investments. At least, not in my book. They should be called tax efficient secured corporate bond investing. But before we can get into my clickbait-y annoying title, we have to get some definitions out of the way!

What is triple net investing? Single tenant triple net lease properties are all around us. If you've ever seen a Starbucks, Taco Bell, O'Reilly's Auto Parts or Walgreens at the corner of Main Street and Main Street in your area, it is usually a property that that particular corporation leases from an investor. A triple net lease is usually used in many different types of real estate asset classes. From retail, to office, to even industrial. It basically means that a tenant is responsible for all of the operating costs of a particular property. The tenant pays for all of the real estate taxes, repairs and maintenance, utilities, insurance, etc. What they pay in rent to the landlord is pure net operating income. The landlord has no operating expenses as it relates to owning the property. Single tenant triple net lease properties are a little different than other types of investment asset classes. If you buy a shopping center with multiple tenants on triple net leases, the landlord usually manages the payment of expenses and takes on the actual property management responsibility and then bills the tenants back for those operating expenses most typically on a pro-rata square footage basis for the maintenance of common areas (Common Area Maintenance or CAM). In the case of single tenant triple net, there is no management responsibility on the part of the landlord. It is truly mailbox money. How these deals usually come about is through the work of real estate developers. A real estate development company will have a relationship with a large corporation's real estate management department. The company will hire the developer to find sites that match very specific criteria. Typically, most retail businesses want to be on heavily trafficked corners in commercial areas with high residential density nearby. This is probably the most valuable real estate in any particular MSA. So you might wonder, "well if it's so valuable, why hasn't it been developed yet?" Many times, if the location is in an already developed area, there will probably already be a structure or structures already built there. This is why you will see an old Taco Bell knocked down and a Burger King built in it's place. I have even seen an older Starbucks get knocked down and literally have a Starbucks get built new across the street! The real estate manager will usually be responsible for achieving some goal of opening "x" amount of stores in a particular region within a particular amount of time. The developer will secure sites that conform to the parameters of the companies new store format, get them approved by that company's real estate department and then get the proposed project entitled by the local government, build it and then lease it back to the company on a long term triple net lease. Very often, the development company will not hold onto the property. They will either sell it immediately or sell it before it's even built, often times for a hefty profit! The reason why they dispose of it quickly is because the property starts to lose value after it becomes occupied by the corporate tenant (We will go into the reasons why later.) The typical buyers of these single tenant triple net leased deals are institutions (there are companies that specialize in buying only these types of assets, see local Rochester company Broadstone Net Lease.) Other buyers might be family offices, high net worth individuals or even insurance companies. The reason why they like triple net is because of the long term predictable cash flow, low management intensity and tax benefits (which I'll go into later.) So, why is it not real estate investing? Simply put you are buying a piece of real estate at a price that far exceeds its replacement cost. The advantage of buying currently existing property is that you can buy it a significant discount to replacement cost which gives you a built in competitive advantage. For example, a couple of years ago, there was a property for sale on 680 Monroe Avenue in Rochester, NY that was occupied by Starbucks. Case study below.

The property was about 2800 square feet, and sold for $868,400, over $300 per square foot! This is in a neighborhood where the price per square foot generally trades at $110 per square foot for existing construction. This is a reason in of itself why I wouldn't like this deal. Also you could build a brand new single story building for around $200 per square foot. So with this deal, most of the value is basically in the lease, not the real estate. Not only that, there was only 7 years left on the Starbucks lease. Beware of these types of deals. Typically the broker will market these properties that have shorter lease durations and be very loud about the fact that the tenant has multiple 10 year lease options or what not.

And that the reason their client is selling is to pursue "other opportunities", otherwise they would hold onto the property, etc. Remember, the seller probably knows more than you. They probably know that Starbucks is only building new stores in tertiary markets like Rochester, NY on highly trafficked corners with drive thrus and with very limited seating. Furthermore, the lease rent of $19.63 a foot double net, is $10 more per foot than similar rent comps in the subject property's location. And those rent comps are either gross plus utilities or modified gross leases. So if Starbucks ended up vacating at the end of their lease, you'd be taking a hair cut on the market lease rent. So how did this story end? Starbucks ended up closing this location (aka going dark). Although the rent is guaranteed by the corporation and will likely be paid through the end of the lease term, you know that the likelihood of them renewing is not likely. The lesson here is, if you are going to consider purchasing a single tenant NNN property, you will want to do some research and due diligence on what corporate store model that company is currently using. You can perform this research quite simply by looking around your market and other comparable markets to see the specifications on what is being currently built and where.

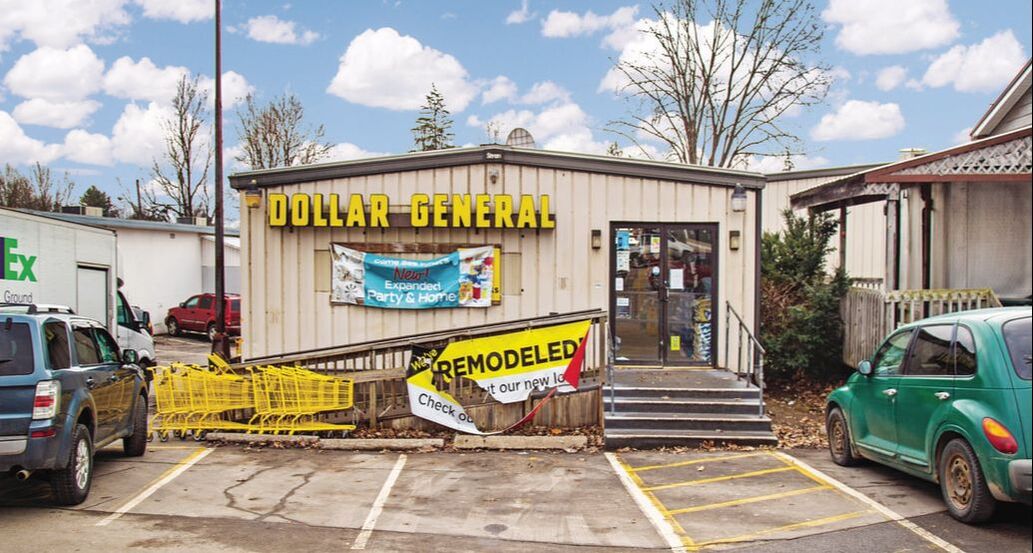

For example, back a few years ago, Dollar General updated it's store format so that it would only consider opening new stores that had at least 8000 square feet, a certain number of parking spots per square foot, ceiling height, etc. The photo above features a Dollar General that is for sale with 2 years left on it's lease. Take a look out there at newly constructed Dollar Generals.

The above DG was built in 2021. It has high ceilings. It is a 9100 square foot stand alone structure with its own large parking lot. When you do research, all stores that have been built since 2020 share similar specifications. So when you compare it to the deal with 2 years left on its lease, you have to think... What would stop a developer from finding a site right down the road and building a brand new Dollar General with the updated store specifications? Sounds like a lot of downside risk and not a lot of upside when considering buying something with not a lot of duration left on the lease.

So now that I have illustrated some of the risks involved with investing in single tenant NNN. There's got to be benefits, right? I mean why would instutional investors like pension funds and life insurance companies have an absolute love affair with this type of product if it was junk. First of all, single tenant NNN is not junk. There are a myriad of benefits but it has a lot of characteristics to it that make it very unlike other forms of real estate investing. The above photo is of a Walgreens NNN deal located in Canandaigua, NY. The price is $7.6 million. It's about 14,000 square feet. It has 10 years left on its current lease and it's current net operating income is $456,000 annually. At an asking price of $522.88 per square foot, why would someone even invest in something like this and pay nearly 5x over other comparable properties? By the way, this property is already sold! The reasons that make an investment like this attractive are as follows:

Things to watch out for in Single Tenant NNN. With all of this bad stuff I said about NNN, I will probably be a buyer of Single Tenant NNN investment properties in the future when I am looking for low management and predicable sources of fixed income. However, I think it is antithesis to many reasons why we invest in real estate. It involves buying a property at a significant premium to replacement cost, which buys you no margin of safety if things go badly. Having a lease with a tenant that is significantly above market rents, which is fine while the tenant is there and paying but not good if things go sideways. So that being said, if you are going to take the plunge and strongly consider investing in single tenant NNN deals, here are some things to watch out for.

Well I hope this answers some questions you might have about a little known investment strategy. If you got value out of this, please register for our monthly newsletter below!

1 Comment

|

AuthorThis blog serves an an outlet for all of our invaluable team members to share their insight on development, property management, and all things affecting real estate in our community. Archives

July 2023

Categories |

RSS Feed

RSS Feed